Software designer

Currently at

iOCO

Researching, prototyping, designing and testing by day, coding, no-coding, launching products by night

Bank Branch Experience

Year

2023

My role

UX/UI Design, Research

Problem

Conduct market research to identify target segments overlooked by traditional banking

Rethinking Banking for Mzansi: My Journey Through the ABSA Hackathon

Back in early 2023, I found myself in one of those long Bank queues you know, the kind that make you question every life choice. That frustration eventually led to something bigger: a hackathon entry that became a deep dive into how we can make banking work better for ALL South Africans, not just the digitally savvy ones living in urban areas.

This project taught me more about inclusive design than any textbook ever could. Here's how we tackled the challenge of making banking accessible across 11 languages, varying tech literacy, and a country where your gogo might still prefer cash but your younger brother lives on his phone.

The Reality Check

The Numbers: 59 million banked South

Africans

The Challenge: 31% still rely primarily

on branches

The Opportunity: 3,800+ physical

locations still serve as community hubs

What I Learned: Just because someone has a smartphone doesn't mean they trust mobile banking. Cultural context matters more than tech specs.

My Goal: Make branch visits feel less like a chore and more like getting help from someone who actually gets your situation.

STEP 1: DEFINE

Getting clear on what we're actually solving (and for whom)

The Problem I Couldn't Ignore

Honest moment: My first instinct was to build an app that would solve everything. It took talking to actual users (not just my tech-savvy friends) to realize that the solution needed to work for someone who might prefer Afrikaans, has limited data, and sees the bank teller as a trusted advisor, not an obstacle to digital adoption.

Business Reality

Almost all major banks are caught between a rock and a hard place: digital transformation pressure vs. customer preference for human interaction.

The constraint: Reduce operational costs without alienating loyal customers who built relationships over decades.

Success Metrics

Reduce wait times: From 23 minutes to under

15

Increase satisfaction: 6.2 to 8.0/10 (being

realistic here)

Language inclusivity: Support for 9

languages (started ambitious, scaled back)

Task completion: 85%+ for users 55+

What I Discovered

This wasn't just about making things digital. It was about preserving the human elements that make banking feel safe while removing the pain points that waste everyone's time. The challenge was finding that sweet spot.

STEP 2: RESEARCH

Getting out of my comfort zone and into real banking queues

What I Actually Did (vs. What I Planned)

Plan: Conduct 5 interviews across 2

provinces in hours.

Reality: Managed 2 meaningful conversations

across JHB.

Sometimes research doesn't go according to plan, and that's

okay.

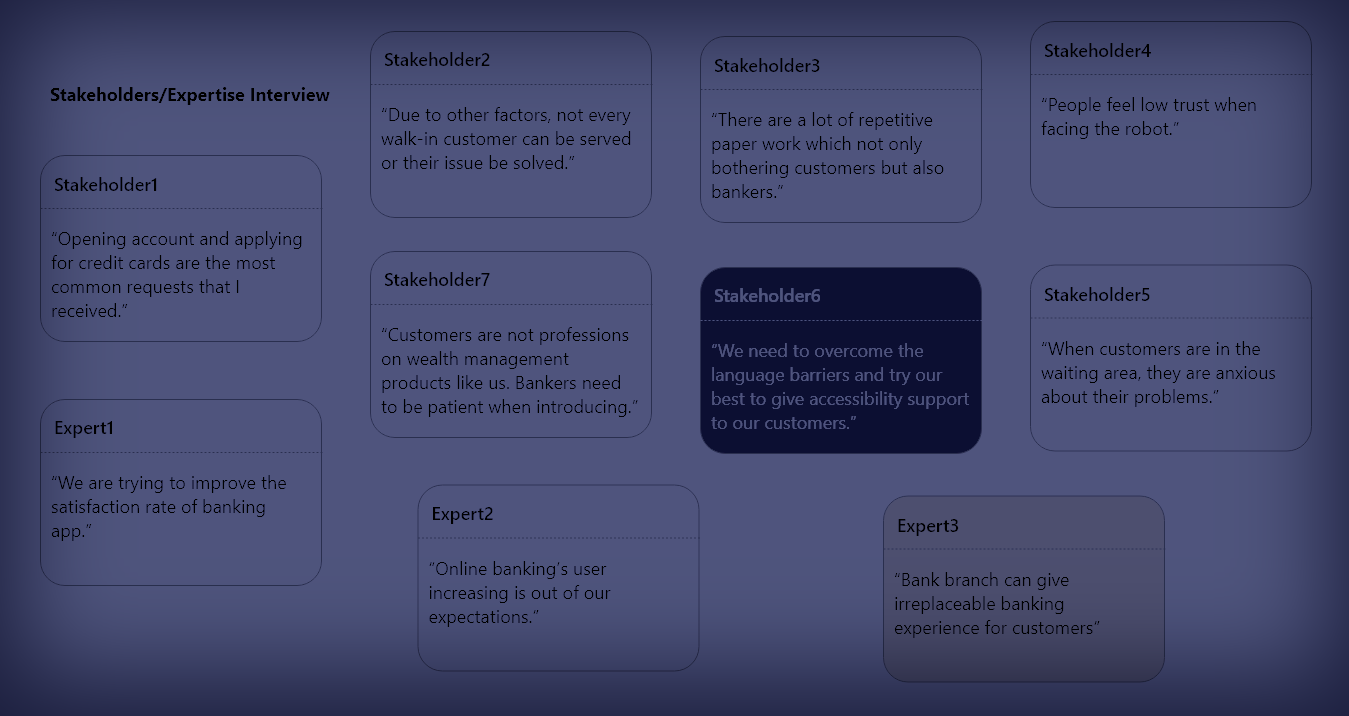

Branch Observations

Spent probably too many hours in bank queues with a notebook (and got some weird looks).

Key insight: The queue isn't just waiting time – it's social time. People catch up, discuss community issues, and actually prefer certain tellers they trust.

Customer Conversations

Surprise finding: Language preference isn't just about understanding – it's about feeling respected.

Staff Insights

Bank staff mostly candid about their frustrations. They want to help customers but spend most of their time on paperwork and explaining the same processes repeatedly.

Aha moment: Staff satisfaction and customer satisfaction are deeply connected.

What I Learned (Sometimes the Hard Way)

The Digital Divide is More Nuanced

- 35% of users have smartphones but prefer branch banking for "important" transactions

- Trust is built through relationships, not features

- Data costs still matter – a lot

- Interface language preference varies by transaction type

Cultural Context Rules Everything

- Banking is often a community activity, especially in townships

- Elderly customers aren't "resistant to change" – they value proven reliability

- Financial decisions often involve extended family input

- Status and respect matter as much as efficiency

Language Reality Check

Started with 11 languages, realized quality over quantity mattered more

STEP 3: ANALYSIS & PLANNING

Making sense of messy research and finding patterns

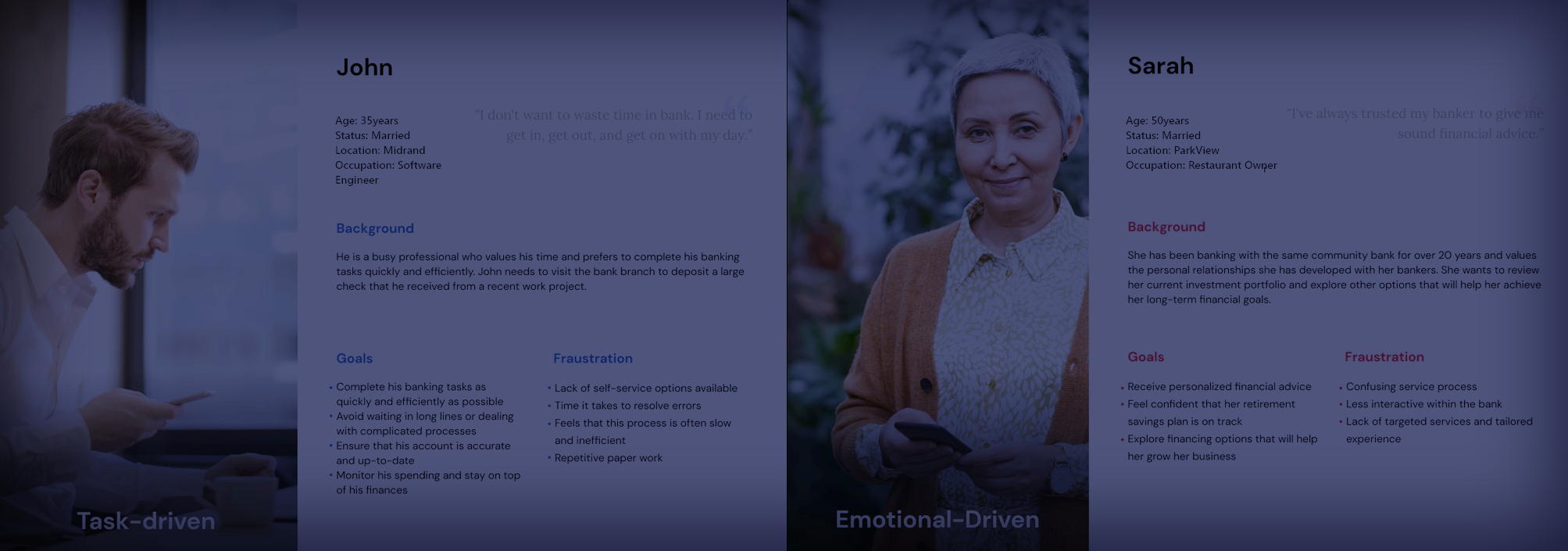

Meet the People Behind the Data

Thabo Mthembu

Age: 34 | Languages: isiZulu, English

The Reality: Works in IT but still prefers seeing a human for anything involving large amounts of money. Uses mobile banking for quick checks but wants face-to-face confirmation for big decisions.

What he told me: "I can code, but when It's my bond payment, I want to look someone in the eye and know it's done properly."

Design implications: Tech literacy ≠ digital trust. Need seamless handoffs between digital and human touchpoints.

Hilary van der Merwe

Age: 41 | Languages: English, Afrikaans

The Reality: She is actually quite tech-savvy (runs the school's WhatsApp group) but doesn't trust banking apps with her pension. Values relationships she's built with bank staff over 20 years.

What she taught me: "It's not about the technology being hard. It's about 20 years of knowing that Priya at the counter understands my needs."

Design implications: Focus on preserving human relationships while reducing administrative friction.

Sipho Lebese

Age: 28 | Languages: Sepedi, English

The Reality: Runs a small transport business, manages cash flow via mobile money but needs branch visits for business banking, loans, and cash deposits. Travels 45 minutes to nearest branch.

What he needs: "I can't afford to make that trip twice because I forgot documents or the system was down."

Design implications: Preparation and reliability are more important than fancy features.

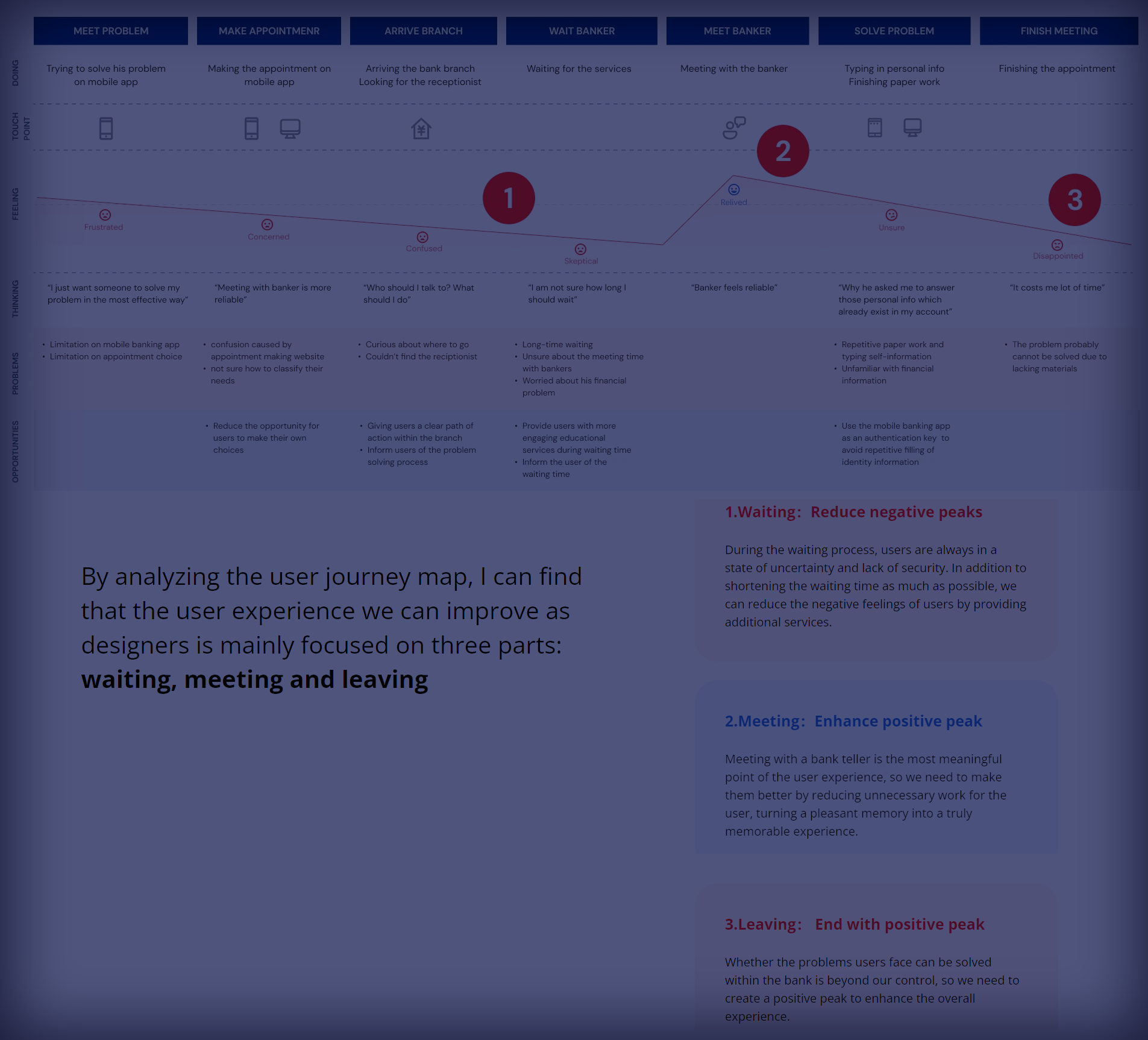

The Journey That Changed My Perspective

I initially mapped the journey from a designer's perspective: neat, linear, logical. Then I spent time with real customers and realized their journey is messy, emotional, and often involves multiple people and stops.

Before Leaving Home (The Anxiety Phase)

Current reality: "Do I have all my documents? What if their system is down again? Should I go early or will I waste my whole morning?"

Opportunity: Pre-visit confidence building through preparation tools and realistic wait time estimates.

What I learned: For rural customers especially, a branch visit is a significant time and cost investment. The anxiety is real.

Arrival & Queue Assessment (The Hope/Dread Moment)

Current reality: "How long is this going to take? Do I have time? Should I come back later?"

Opportunity: Clear communication and alternative options based on wait times and transaction complexity.

Insight: People make emotional decisions about whether to stay or leave within the first 2 minutes of arriving.

Getting Help (The Trust-Building Phase)

Current reality: Either great (you get someone who knows you) or frustrating (explaining your situation from scratch to someone who seems rushed).

Opportunity: Better staff preparation and customer context, without sacrificing privacy.

Walking Away (The Reflection Moment)

Current reality: "Did I really need to come here for this? Will I remember what they told me?"

Opportunity: Clear next steps and educational content that builds confidence for future self-service.

STEP 4: DESIGN

Turning insights into solutions (with several iterations)

Design Principles That Actually Mattered

Honest moment: My first design principles were very pretty and completely generic. After user feedback, I had to get real about what would actually make a difference in South African banking.

What I Learned to Prioritize

- Confidence over speed: People need to feel sure about their actions

- Choice over force: Digital assistance, not digital replacement

- Context over features: Solutions that fit real life, not ideal scenarios

- Relationships over efficiency: Preserve what people value about human interaction

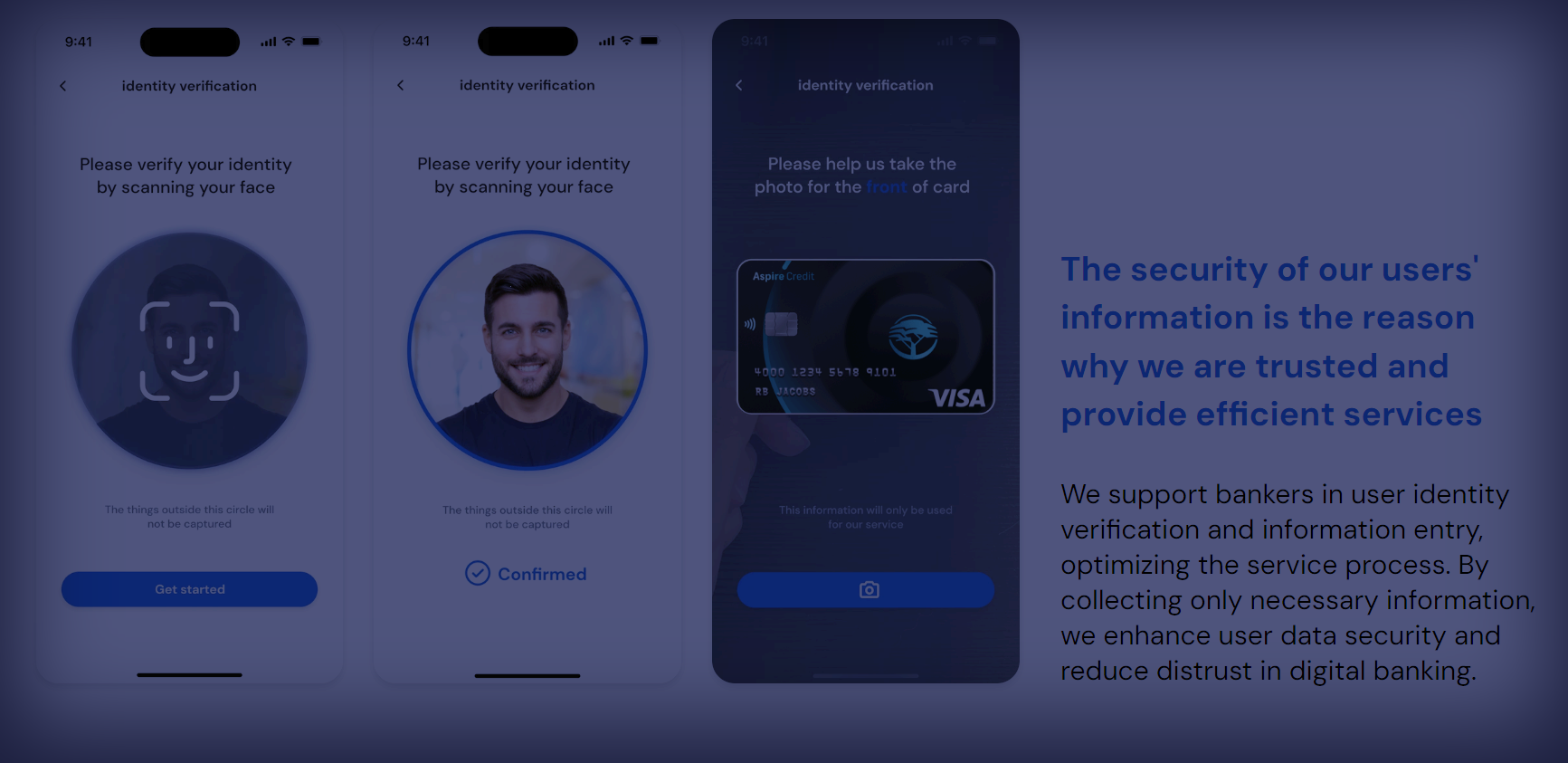

The Solution Strategy

- Smart preparation: Help people come ready, not just show up

- Transparent queuing: Real information about wait times and complexity

- Assisted self-service: Technology that makes staff more helpful, not less needed

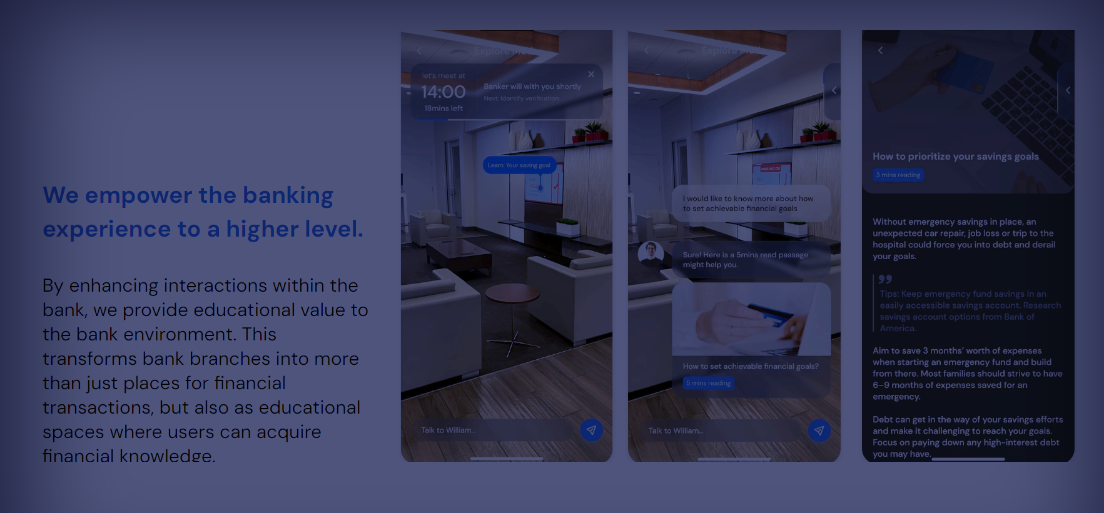

- Contextual education: Learning opportunities built into transactions

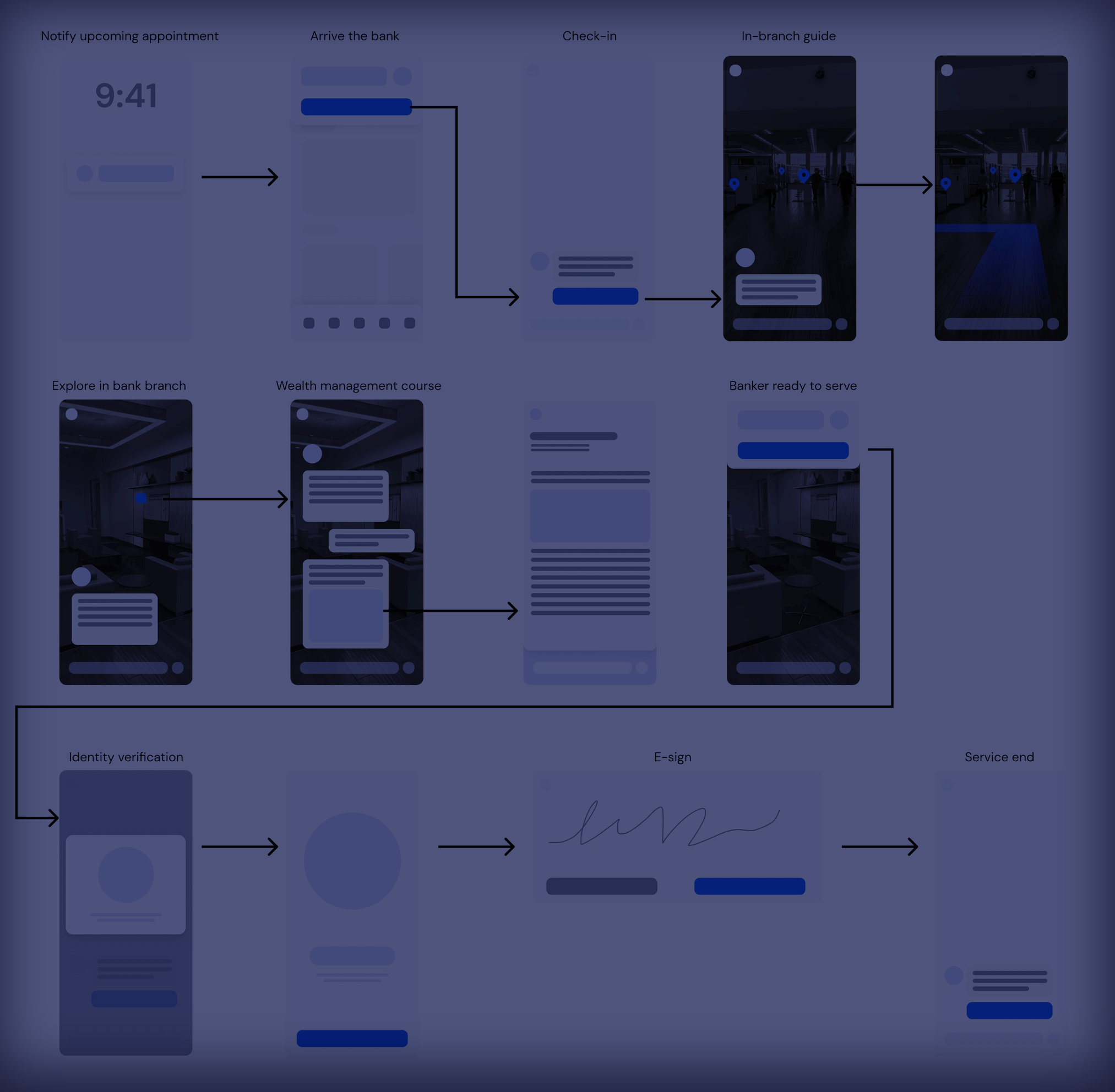

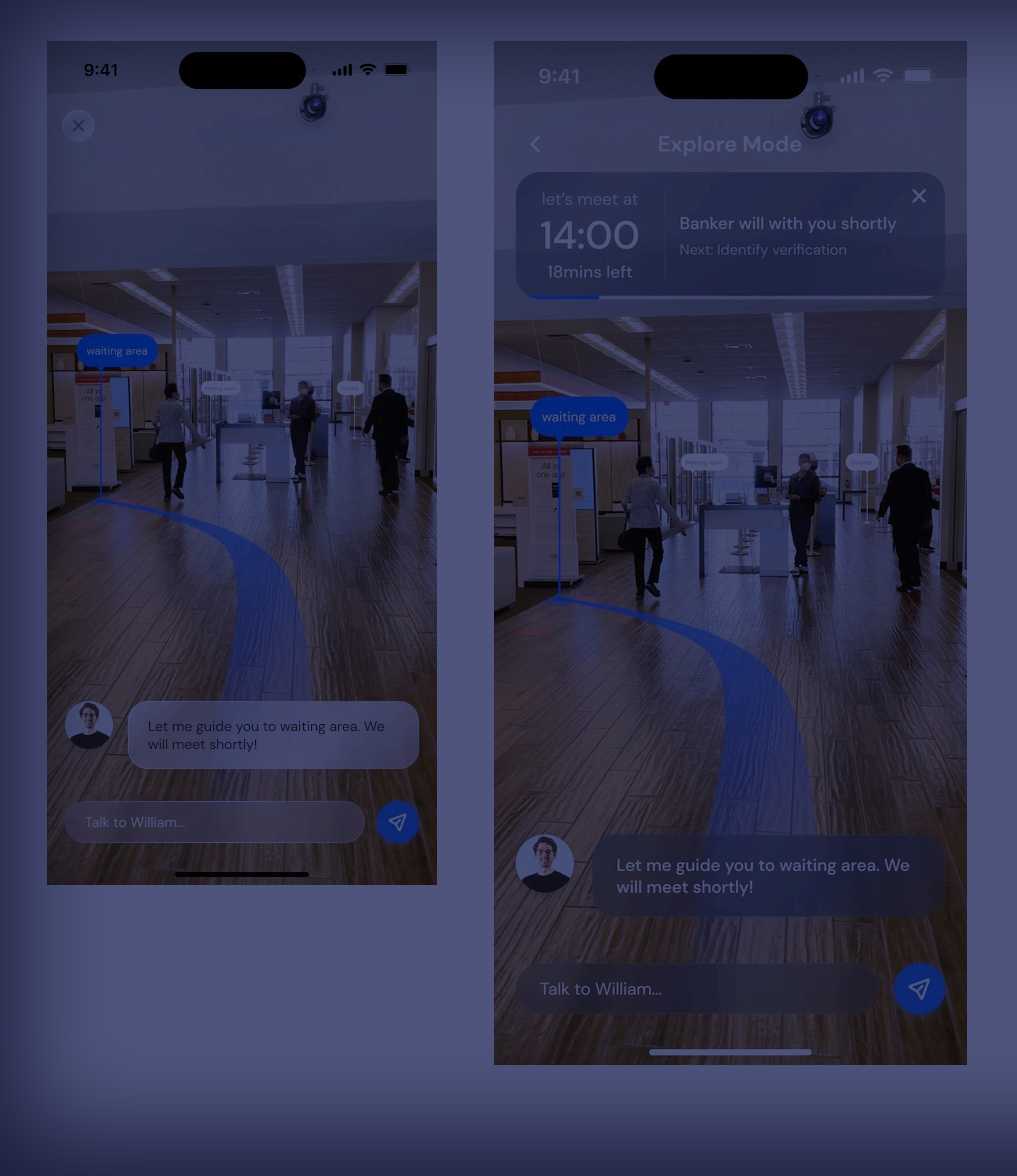

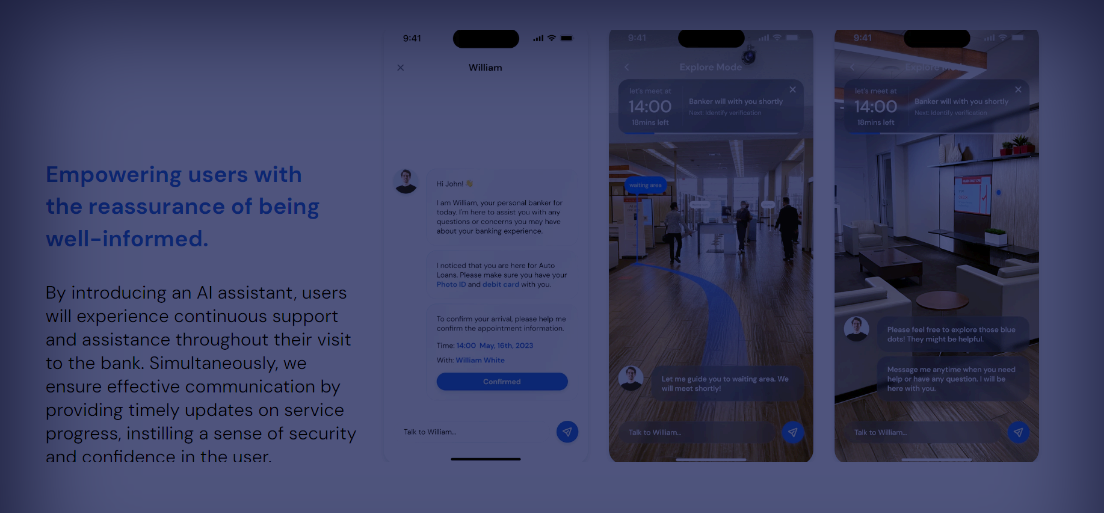

Queue Intelligence

Not just wait times, but "come back at 2pm for a 5-minute wait" recommendations

Preparation Assistant

Transaction-specific document checklists and step-by-step prep guides

Cultural Concierge

Matching customers with staff based on language and cultural preferences (when possible)

Progressive Trust

Gradually building digital confidence through positive experiences

STEP 5: PROTOTYPING

Building to learn, not to impress

Prototype Evolution (What Actually Worked)

Started with high-fidelity mockups because they look impressive. Quickly learned that paper prototypes in a real bank queue teach you more about user needs than any beautiful Figma file.

Paper & Conversations

Sketched basic flows on paper and tested them with 2mentors about actual bank queues and I received generous feedback.

Key insight: People's mental models of "preparation" were very different from my assumptions.

Interactive Prototypes

Built clickable prototypes in Figma and tested with mentors. Learned more from that testing than any formal usability test.

Reality check: Voice navigation was popular in concept, challenging in practice with ambient noise.

Wizard of Oz Testing

Simulated the "smart queue" system manually for a few days, updating wait times by hand. Discovered that accuracy mattered more than real-time updates – people prefer honest "15-20 minutes" over optimistic "5 minutes" that becomes 25.

STEP 6: TESTING

Learning from real people in real situations

Testing Reality vs. Research Plans

Planned: Controlled usability sessions with 3 mentors

What I Measured

- Task completion: Can people actually do what they came to do?

- Emotional response: Do they feel more confident or more frustrated?

- Trust indicators: Would they use this with their own money?

- Cultural comfort: Does it feel "for them" or "for other people"?

Results That Surprised Me

- Task completion: 73% → 87% (better than expected)

- Time to complete: Actually increased by 5% initially (people were more thorough)

- Confidence score: 6.1 → 7.8/10

- Return intention: 89% said they'd use it again

STEP 7: ITERATION

What I'm still learning from ongoing usage

The Interface That Emerged

These aren't the polished screens I started with. They're the ones that actually worked after few hours of iteration with mentors

What This Project Taught Me About UX

Things I Got Right (Eventually)

- Starting with people, not personas: Real conversations beat assumption-based user profiles every time

- Designing for trust, not just usability: In financial services, emotional comfort matters as much as task completion

- Embracing constraints: Data costs, language diversity, and infrastructure limitations weren't problems to solve but realities to design for

- Measuring what matters: User confidence turned out to be more predictive of success than traditional UX metrics

Mistakes I'm Still Learning From

- Overestimating appetite for digital: Just because someone can use technology doesn't mean they want to for everything

- Underestimating cultural nuance: Language support isn't just translation – it's understanding different cultural approaches to financial decision-making

- Perfect vs. good enough: Spent too much time polishing features that users found unnecessary

- Implementation reality: Banking technology moves slowly for good reasons, and that's something to design around, not fight

The biggest shift in my thinking: Good UX in emerging markets isn't about bringing "global best practices" to local markets. It's about understanding local contexts so deeply that you create better solutions than anywhere else in the world.

Final Thoughts

"This project changed how I think about inclusive design. It's

not about making one solution work for everyone – it's about

creating systems that respect how different people prefer to do

things." — Me, reflecting after 8 hours

This project taught me that designing for South Africa's

diversity requires humility, curiosity, and a willingness to

abandon assumptions. The best design doesn't impose solutions—it

amplifies what already works while removing what doesn't.